Helping Military Families, VA Buyers & Home Sellers in Pensacola, FL

Work with Vivian Corwin, a trusted Pensacola real estate agent specializing in VA loans, relocation, and smooth home sales.

HOW IT WORKS

A Simple, Stress-Free Process from Start to Finish

Consultation – We discuss your goals and timeline

Strategy – I create a custom plan tailored to your needs

Marketing / Home Search – Maximum exposure for sellers or targeted home search for buyers

Negotiation – I work to get you the best terms and price

Closing – Smooth process all the way to the finish line

⭐ MRP | PSA | CREN | CBDA | Equal Housing

Trusted by military families & homebuyers across Pensacola

HI I’M VIVIAN

Vivian Corwin

Realtor SL#3406257

I’m Vivian Corwin

A Pensacola real estate agent helping buyers and sellers navigate the market with confidence, clarity, and results.

WHY WORK WITH ME

Expert Guidance You Can Trust

Local Pensacola market expert

Military relocation specialist

Proven marketing strategies that get results

Strong negotiation to protect your investment

Clear communication every step of the way

Thinking About Relocating to Pensacola, Florida?

Explore Pensacola, Pace, Milton, and nearby Gulf Coast communities with local insights, lifestyle highlights, and expert relocation guidance.

WHO I HELP?

Military Relocation

Helping military families relocate to Pensacola, Pace, and surrounding areas with a smooth, stress-free process.

VA Loan Buyers

Guiding buyers through VA loan options and helping them make the most of their benefits.

First-Time Homebuyers

Step-by-step support for buyers who are new to the process and want to feel confident.

New Construction Buyers

Helping you navigate builder contracts, upgrades, and inspections so you don’t overpay.

Not sure where you fit? Let’s talk about your goals.

HI I’M VIVIAN

Vivian Corwin

Realtor SL#3406257

I’m Vivian Corwin

A Pensacola real estate agent helping buyers and sellers navigate the market with confidence, clarity, and results.

WHY WORK WITH ME

Expert Guidance You Can Trust

Local Pensacola market expert

Military relocation specialist

Proven marketing strategies that get results

Strong negotiation to protect your investment

Clear communication every step of the way

FEATURED AREAS

Explore Homes in Top Pensacola Communities

WHO I HELP?

Military Relocation

Helping military families relocate to Pensacola, Pace, and surrounding areas with a smooth, stress-free process.

VA Loan Buyers

Guiding buyers through VA loan options and helping them make the most of their benefits.

First-Time Homebuyers

Step-by-step support for buyers who are new to the process and want to feel confident.

New Construction Buyers

Helping you navigate builder contracts, upgrades, and inspections so you don’t overpay.

Not sure where you fit? Let’s talk about your goals.

READY TO MAKE YOUR MOVE?

Whether you're buying, selling, or relocating, I’ll guide you every step of the way.

⭐ 5-Star Rated | 📍 Pensacola Local Expert | 🎖 Military Relocation Specialist

Frequently Asked Questions About Buying & Selling in Pensacola, FL

How do VA loans work when buying a home in Pensacola, Florida?

VA loans are one of the most common ways military families buy homes in Pensacola, Florida. They allow eligible buyers to purchase with no down payment and competitive interest rates.

What are the best areas to live near NAS Pensacola or Whiting Field in Florida?

The most popular areas include Pensacola, Pace, Milton, Gulf Breeze, and Navarre, depending on your commute, schools, and lifestyle preferences.

How much is my home worth in Pensacola, Pace, or Milton, Florida right now?

Home values in Pensacola, Pace, and Milton depend on location, condition, and current market trends. A local market analysis provides the most accurate estimate.

What should I do to prepare my home for sale in Pensacola, Florida?

To prepare your home for sale in Pensacola, focus on decluttering, deep cleaning, minor repairs, and curb appeal to attract serious buyers.

Can I buy or sell a home while relocating to or from Pensacola, Florida?

Yes. Many buyers and sellers successfully complete transactions remotely using virtual tours, video walkthroughs, and local expert guidance.

WHAT MY CLIENTS ARE SAYING

Trusted by Buyers & Sellers Across Pensacola

Pensacola Real Estate Tips & Updates

How to Decide Between Pace, Milton, and Cantonment

Compare Pace, Milton, and Cantonment to find the right community for your lifestyle and budget. ...more

Buying a Home

July 15, 2026•3 min read

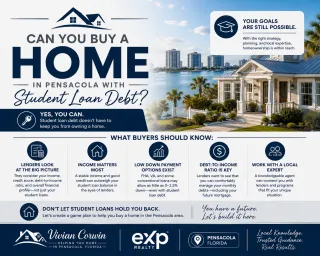

Can You Buy a Home in Pensacola With Student Loan Debt?

Learn how student loan debt can affect your ability to buy a home in Pensacola. ...more

Buying a Home

July 13, 2026•3 min read

What Buyers Should Know About Older Homes in Pensacola

Learn what buyers should know before purchasing an older home in Pensacola. ...more

Buying a Home

July 10, 2026•2 min read

Follow me on Social Media